By David C. D’Albero II

No matter where you are on your financial journey—whether just beginning to build wealth or firmly established—having the right legal documents in place is critical. These foundational tools not only protect your assets but also ensure your loved ones are cared for, no matter what life throws your way.

Here’s a breakdown of the five essential legal documents that every adult should have to safeguard their legacy and avoid unnecessary stress for their families.

- A Will: Your Plan for the Future

A will is often the first legal document that comes to mind in estate planning—and for good reason. It outlines your wishes for how your assets will be distributed after your passing. But its importance goes beyond just dividing wealth.

- Protect Minor Children: A will allows you to designate guardians for your minor children, ensuring they are cared for by someone you trust.

- Avoid Probate Chaos: Without a will, the state determines how your assets are distributed, which can lead to disputes and lengthy court proceedings.

Don’t assume a will is only for the wealthy. Even modest estates benefit from having a clear, legally binding plan in place.

- Durable Power of Attorney: Financial Protection When You Need It Most

A durable power of attorney allows you to name someone to manage your finances if you become incapacitated. This trusted individual can handle bills, investments, and other financial matters on your behalf.

Without this document, your family might need court approval to manage even basic financial responsibilities, adding unnecessary delays and stress. A durable power of attorney serves as a financial safety net, ensuring your affairs run smoothly even in challenging times.

- Healthcare Proxy: Giving a Voice to Your Medical Choices

Who will make medical decisions for you if you’re unable to? A healthcare proxy gives someone you trust the legal authority to ensure your wishes are followed.

- Reduce Stress for Loved Ones: This document spares your family from having to guess your preferences in critical moments.

- Align with Your Wishes: It ensures decisions about treatments, surgeries, or other medical care align with what you would have wanted.

- Living Will: Your Voice When You Can’t Speak

A living will works hand-in-hand with your healthcare proxy by specifying your preferences for medical treatment if you’re unable to communicate. This document addresses sensitive issues like:

- Resuscitation

- Life support

- Organ donation

By having a living will, you ensure that your values are honored while easing the emotional burden on loved ones who might otherwise have to make difficult choices on your behalf.

- Revocable Trust: Flexibility and Privacy

Often overlooked, a revocable trust is a powerful tool for managing your assets both during your lifetime and after.

- Avoid Probate: Assets in a revocable trust transfer to beneficiaries without going through probate, saving time and money.

- Maintain Privacy: Unlike a will, trust details don’t become public record, offering a layer of confidentiality.

- Simplify Multistate Property Management: A revocable trust is particularly beneficial for those with property or investments in multiple states.

This flexible, secure document can make estate planning far more efficient for families, ensuring your wishes are carried out seamlessly.

The Bottom Line: Protect Your Legacy Today

These five legal documents form the foundation of a sound financial and legal plan. Having them in place gives you confidence that your assets will be protected, your wishes honored, and your loved ones supported.

Don’t wait for a crisis to begin planning. If you need help getting started, Strata Capital is here to guide you every step of the way. Our personalized approach ensures your plan fits your unique circumstances, offering peace of mind for today and tomorrow.

Strata Capital is a wealth management firm serving corporate executives, professionals, and entrepreneurs in the New York Tri-State Area, focusing on corporate benefits and executive compensation. Co-founded by David D’Albero and Carmine Coppola, the firm specializes in making the complex simple to ensure clients feel confident in their financial decisions. They can be reached by phone at (212) 367-2855, via email at carmine@stratacapital.co, or by visiting their website at stratacapital.co.

Cornerstone Planning Group, Inc., (“CSPG”) is an SEC registered investment advisory firm. The information contained herein should not be construed as personalized investment advice and should not be considered as a solicitation for investment advisory service. The information (e.g., tax ) provided is believed to be accurate however CSPG does not guarantee or otherwise warrant such information. For more information regarding CSPG you can refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov) and review our Form ADV Brochure and other disclosures.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

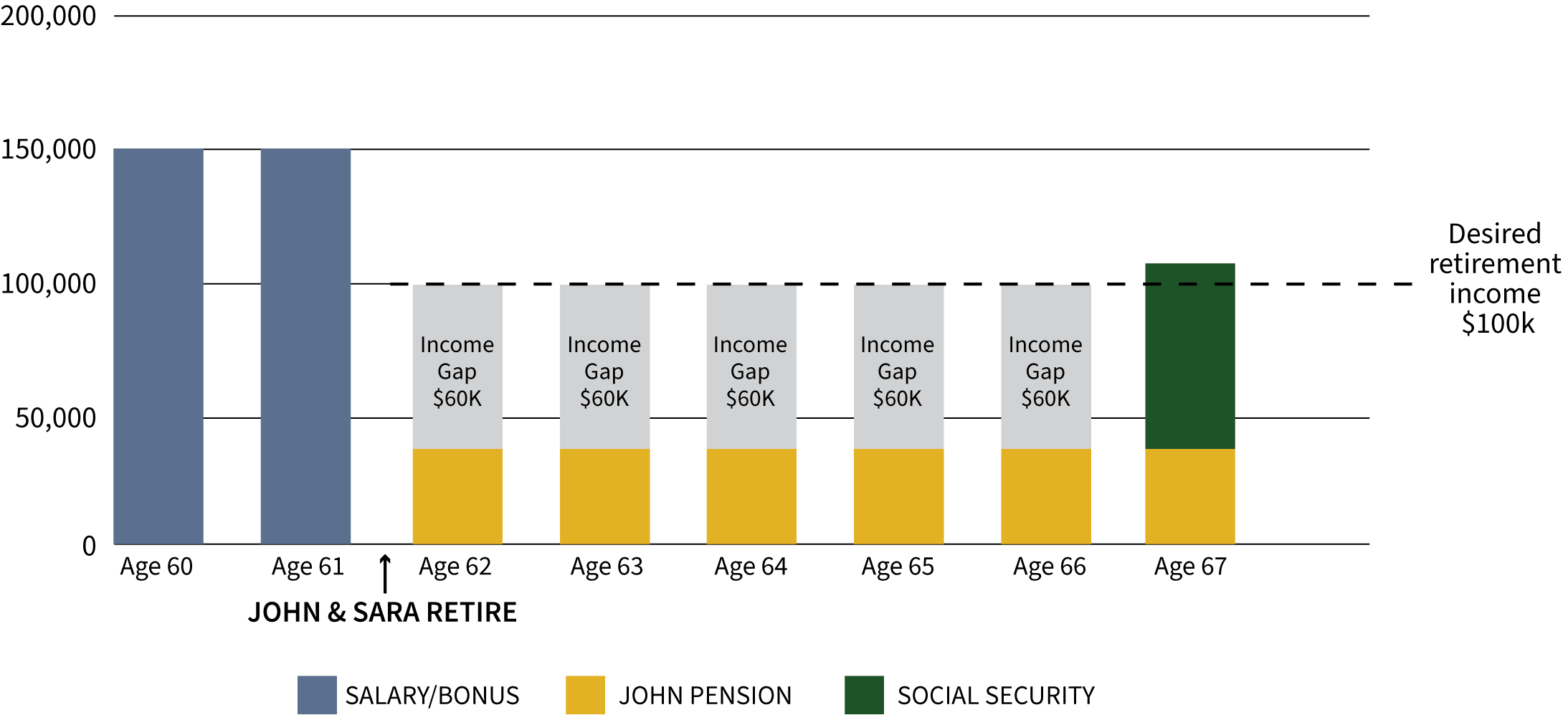

You can see that John and Sara will have an income gap of $60,000 for the five years before Social Security kicks in. They will have to pull this from retirement accounts or other investments, which can lead to depleting assets sooner than anticipated.

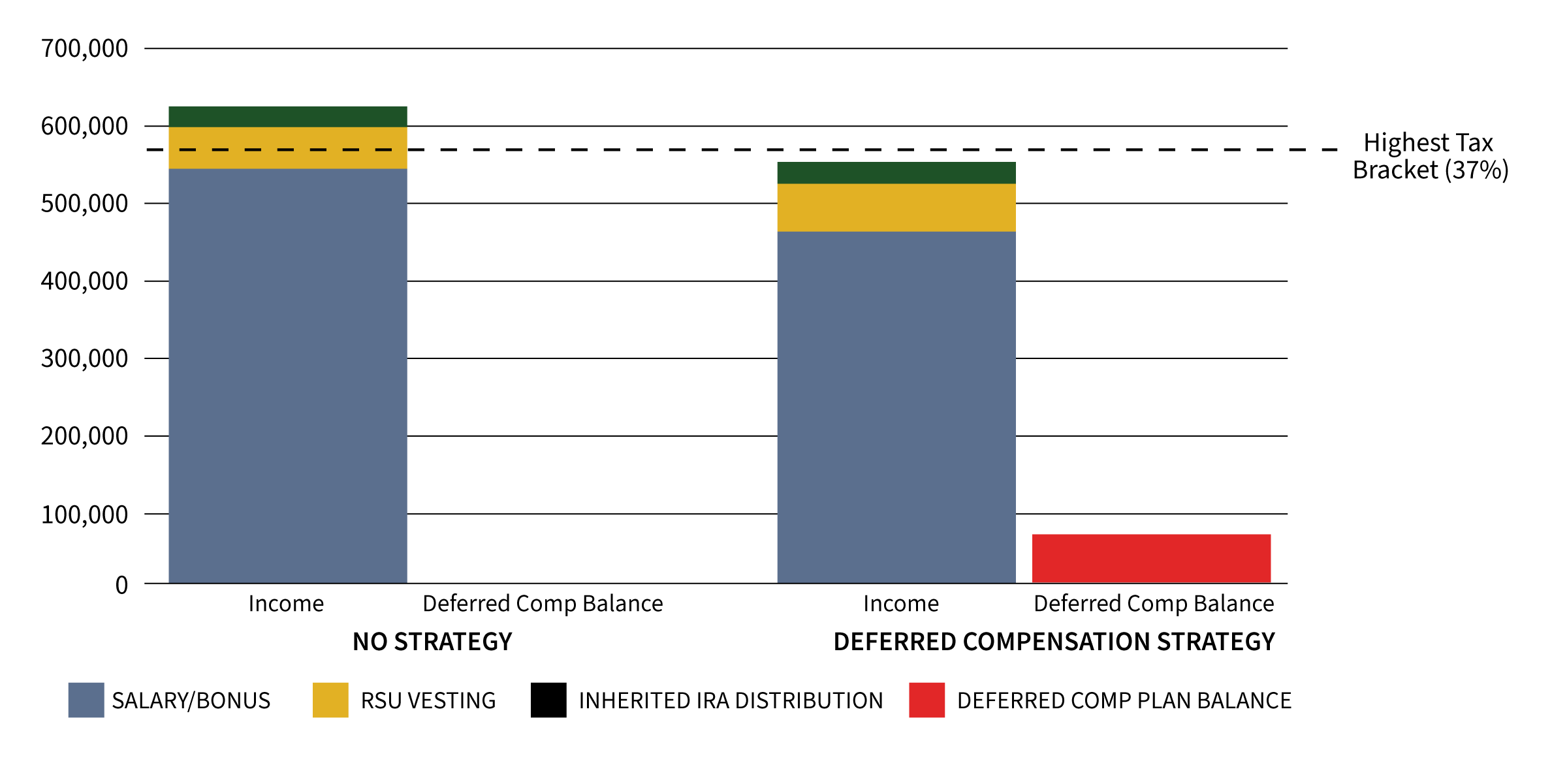

You can see that John and Sara will have an income gap of $60,000 for the five years before Social Security kicks in. They will have to pull this from retirement accounts or other investments, which can lead to depleting assets sooner than anticipated. The gap they previously had to make up is now filled by Sara’s distributions from her deferred comp plan. This has a significantly positive impact on their future because now the couple can let their retirement and investment assets continue to grow over the five-year period and use those gains later to supplement their income.

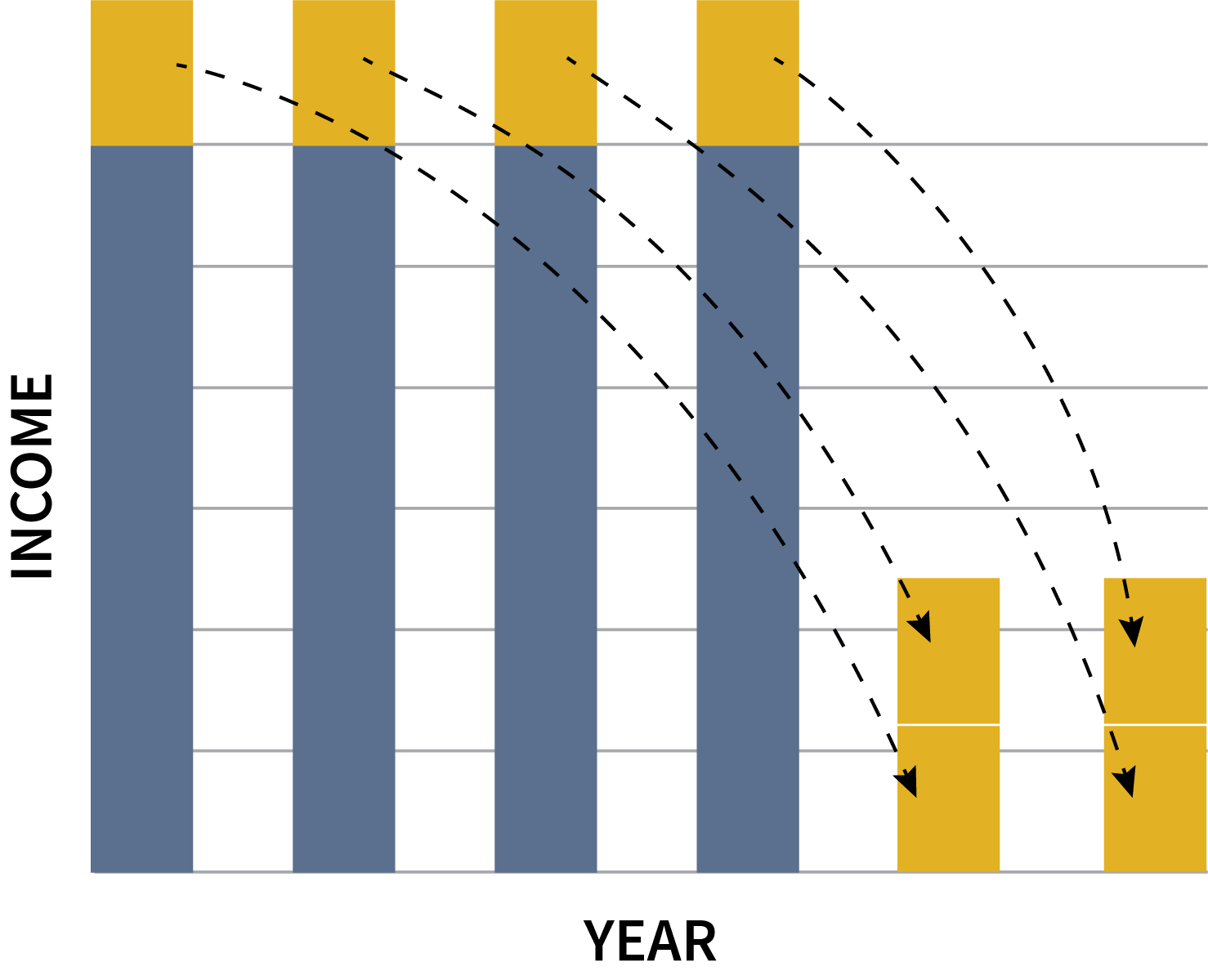

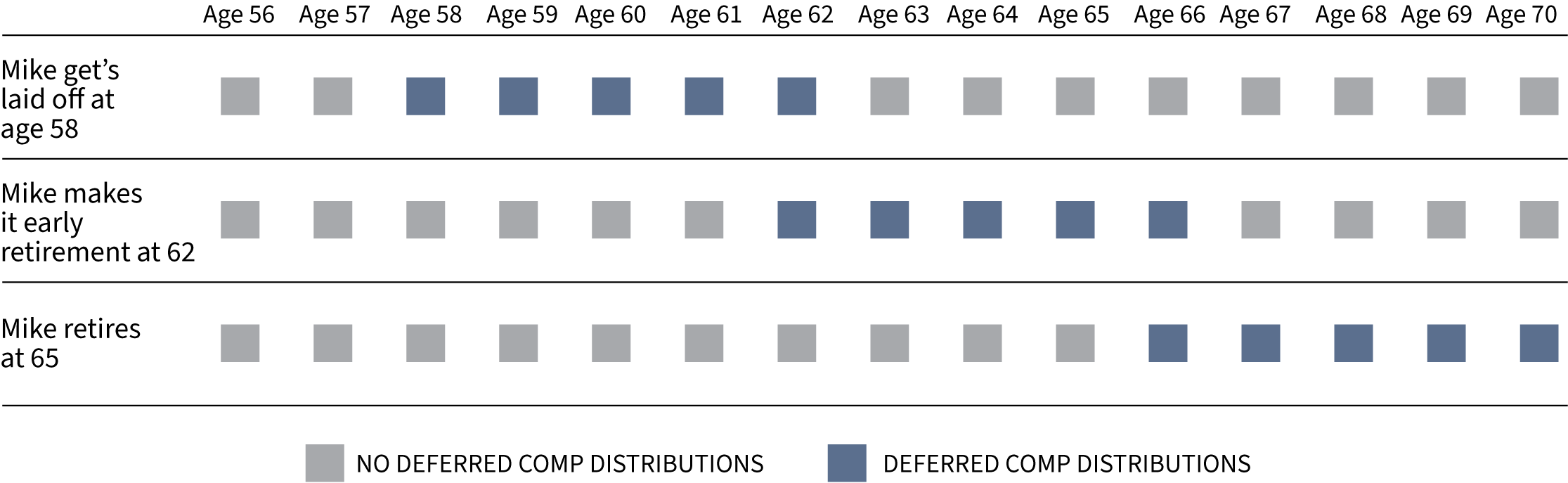

The gap they previously had to make up is now filled by Sara’s distributions from her deferred comp plan. This has a significantly positive impact on their future because now the couple can let their retirement and investment assets continue to grow over the five-year period and use those gains later to supplement their income.  Looking at this chart, you can see that no matter when Mike leaves MetLife, he has a purpose for his deferred compensation. If he gets laid off at 58 (or any age, for that matter), the deferred comp will pay out over the next five years. Being that the current value is $350,000, that could be around $70,000 in income each year. This will allow him to buy some time while he looks for another job, or he could accept a job making less money since he has this income to supplement his pay.

Looking at this chart, you can see that no matter when Mike leaves MetLife, he has a purpose for his deferred compensation. If he gets laid off at 58 (or any age, for that matter), the deferred comp will pay out over the next five years. Being that the current value is $350,000, that could be around $70,000 in income each year. This will allow him to buy some time while he looks for another job, or he could accept a job making less money since he has this income to supplement his pay.