Retirement is expensive. If you want to recreate your income in retirement, you’ll need to save an average of 10-15% of your income throughout your career. But it’s no secret that most people either get started late or find themselves tracking behind their targets late in the game. At some point, you may realize that hitting your numbers might require being more aggressive than planned. But how should you go about doing this? One of the most overlooked and underutilized strategies available for employees to get on track is the 401(k) after-tax contribution.

What Are 401(k) After-Tax Contributions?

In addition to the traditional pre-tax and Roth contributions, most plans also allow for 401(k) after-tax contributions. It’s called “after-tax” because the money contributed has already been subjected to income tax at the time of deposit, which means it doesn’t provide an immediate tax deduction like pre-tax contributions. However, the earnings on after-tax contributions grow tax-deferred within the 401(k) account, just like pre-tax contributions. They are also subject to income tax when withdrawn in retirement.

So Why Use 401(k) After-Tax Contributions?

1. Higher Contribution Limits

The IRS has annual contribution limits for 401(k) plans, which include a limit on pre-tax and Roth contributions. The combined limit for 2023 pre-tax and Roth contributions is $22,500 per year, or $30,000 if you’re age 50 or older.

However, 401(k) after-tax contributions allow you to save more for retirement if you have the means to do so. The 2023 401(k) total contribution limit, including after-tax contributions, is much higher—up to $66,000 or 73,500 for those aged 50 or older.

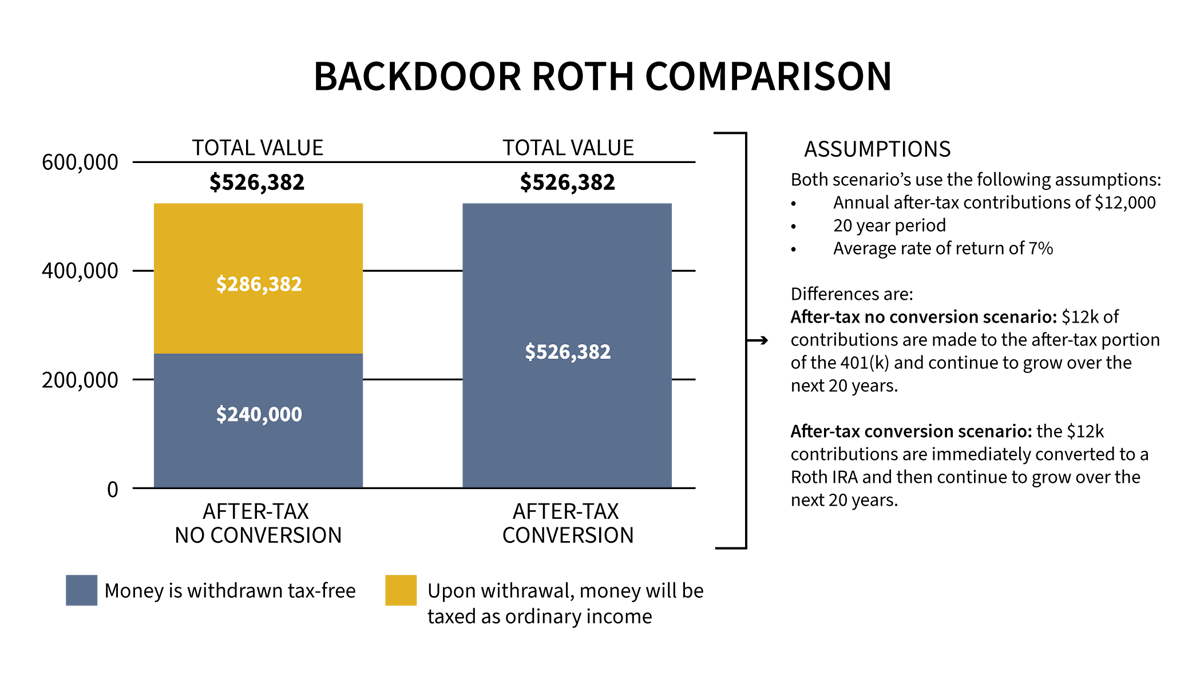

2. Conversion to Roth

You can convert your 401(k) after-tax contributions into a Roth IRA or Roth 401(k) when you leave your job or if your plan allows in-service conversions. Some plans will even let you do this internally.

Roth conversions can be valuable for building a tax-free retirement income stream. Since after-tax contributions have already been taxed, the conversion to a Roth account won’t trigger additional taxes.

There’s only one exception to consider: if you’ve generated earnings on your after-tax contributions, which may happen if the funds have been sitting in the account for a while. This doesn’t mean you can’t do the conversion; it simply means that those earnings must be rolled into a traditional IRA to avoid taxation.

In short, your contributions can go to the Roth account, and any earnings will go to a traditional pre-tax IRA.

3. Tax-Deferred/Tax-Free Growth

Much like pre-tax and Roth contributions, 401(k) after-tax contributions can grow tax-deferred until you withdraw the funds in retirement. This means your retirement savings have the opportunity to grow more efficiently over time.

If your plan permits, you may be able to move the funds to a Roth account shortly after you’ve made your contribution. This is called a mega backdoor Roth. Funds will have the opportunity to grow not only tax-deferred, but the withdrawals will also be tax-free. Check out our blog on back-door Roth contributions to learn more about this strategy.

4. Employer Match

If you’re not taking full advantage of your employer match, you’re leaving lots of money on the table. Some employers provide a matching on 401(k) after-tax contributions, similar to how they match pre-tax contributions.

Remember, an employer match provides an immediate return on your investment, so check into your employee benefits and make certain you aren’t missing out on this valuable perk.

Are You Considering 401(K) After-Tax Contributions?

As a strategy, 401(k) after-tax contributions can considerably impact a retirement savings plan. But before you begin contributing, review your current cash flow to determine whether contributing extra dollars is reasonable. Prioritizing your family’s stability is key. While making sacrifices can lead to rewards, it’s essential first to secure your emergency savings and meet your immediate needs.

Before making any decisions, remember that company rules and federal laws governing 401(k) plans can change. If you’d like to discuss your situation with a financial advisor, schedule a meeting with us. Together, we can explore how after-tax 401(k) contributions can enhance your overall retirement and tax planning strategy. Let’s connect and discuss how we can optimize your financial future.

Strata Capital is a wealth management firm serving corporate executives, professionals, and entrepreneurs in the New York Tri-State Area, focusing on corporate benefits and executive compensation. Co-founded by David D’Albero and Carmine Coppola, the firm specializes in making the complex simple to ensure clients feel confident in their financial decisions. They can be reached by phone at (212) 367-2855, via email at carmine@stratacapital.co, or by visiting their website at stratacapital.co.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

This material was prepared by Crystal Marketing Solutions, LLC, and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate and is intended merely for educational purposes, not as advice.