By Carmine Coppola

MetLife offers a lucrative benefits package; it’s one of the biggest advantages of working for the company. When it comes to retirement savings opportunities, especially, your available options are remarkably better than what the majority of employers offer. But many MetLife employees are unfamiliar with a plan that sets their benefits apart from most: the MetLife Leadership Deferred Compensation Plan.

This plan allows eligible employees at salary grades 10S to 13S, such as Assistant Vice Presidents and MetLife company officers, earning over $345,000 in total compensation for 2024 (determined by the IRS and may change yearly), to defer salary or bonus payments.

You’re probably already familiar with the 401(k), Personal Retirement Account (PRA), and traditional pension (for the tenured folks) and how they can benefit your financial well-being. The MetLife Leadership Deferred Compensation Plan is a lesser-known and far more flexible tool. It is a nonqualified deferred compensation plan (NQDC), also known as an elective deferral or supplemental executive retirement plan.

In this article we’ll give you a brief overview of how the plan works and then share four reasons why you need to begin utilizing it to your advantage, starting today.

What Makes the MetLife Leadership Deferred Compensation Plan Different?

There’s far more to this plan than you might think.

The MetLife Leadership Deferred Compensation Plan allows you to put away and invest an uncapped amount each year, reducing your taxable income by the amount you defer. You can also enjoy tax-deferred investment growth until distribution, with flexibility on when you start receiving distributions — at retirement or sooner if you want to align payouts with other earlier financial goals. And distributions are taxed at ordinary income tax rates, so imagine how you can use this strategically alongside your tax planning.

These deferred compensation plans also allow you to pick investments and can even qualify for a company match; consider this a raise! But unlike a 401(k) plan, a nonqualified deferred compensation plan places no limits on your contributions, no age restrictions on withdrawals, and no required minimum distributions.

So, how does this work?

How Deferments Work

MetLife permits you to defer your base salary, Annual Variable Incentive Compensation Plan or successor annual cash bonus plan or program (AVIP), sales incentive compensation, and/or performance shares. Minimum deferrals are 5% and max limits are 75% of your base salary with AVIP and Sales Incentive Performance Shares at 100%.

How the Company Match Works

Not only does participation allow for taking advantage of the tax benefit, but compensation deferrals are also eligible for company contributions through the MetLife Auxiliary Match Plan. The match is the same as the 401(k), with a maximum company match of 4% of compensation. For more details on the Auxiliary Match, you can visit our MetLife page where we give an overview of how that works.

How Distributions Work

When making contributions to the NQDC, you choose when and how distributions happen — meaning, you can tie distribution to a specific date or event, like a retirement date or layoff. And you also choose how the payment is received: lump sum or up to 15 annual installments. Again, distributions are taxed at ordinary income tax rates.

How Investing Works

NQDC contributions are not actually invested into funds in the way your 401(k) investments are. Instead, you choose which tracking funds to track and the plan balance will adjust according to the performance of those funds. MetLife currently offers 11 different tracking funds, each of which mirrors the performance of an index or actual fund. (Reference your guide to see what funds are available.)

Key Considerations in MetLife Leadership Deferred Compensation Planning

Key Considerations in MetLife Leadership Deferred Compensation Planning

It’s gratifying to know you work for a solid employer who values your contributions and wants you to stick around. However, you have some critical decisions when you elect to participate in a deferred compensation plan. Participation typically involves adhering to a designated enrollment period and establishing a written agreement with MetLife.

This plan agreement outlines crucial details, such as the amount of income to be deferred, the deferral period or schedule of distributions, and your investment choices. Once elections are made, they can be difficult or impossible to change, so you don’t want to go into this lightly.

With so many possibilities and so much at stake, deferred comp plans can feel overly complex and even intimidating. The best way to start thinking about your strategic approach is to break it down into three main components:

- What do you want to use the deferred compensation for?

- How much of your salary or bonus will you defer each year?

- When do distributions from the plan start, and how long do they last?

Before moving forward, understanding your options and looking at the big picture is vital

We will explore four situations in which you can confidently and strategically leverage your MetLife Leadership Deferred Compensation Plan.

Strategy 1: Tax Reduction

Deferrals into your MetLife Leadership Deferred Compensation Plan lower your taxable income in the year you defer income. So, if your total compensation was $400,000 and you decided to defer $25,000, your annual income would be $375,000.

A common strategy we use is offsetting other income, such as stock compensation or inherited IRA withdrawals, with deferred comp.

Let’s look at an example.

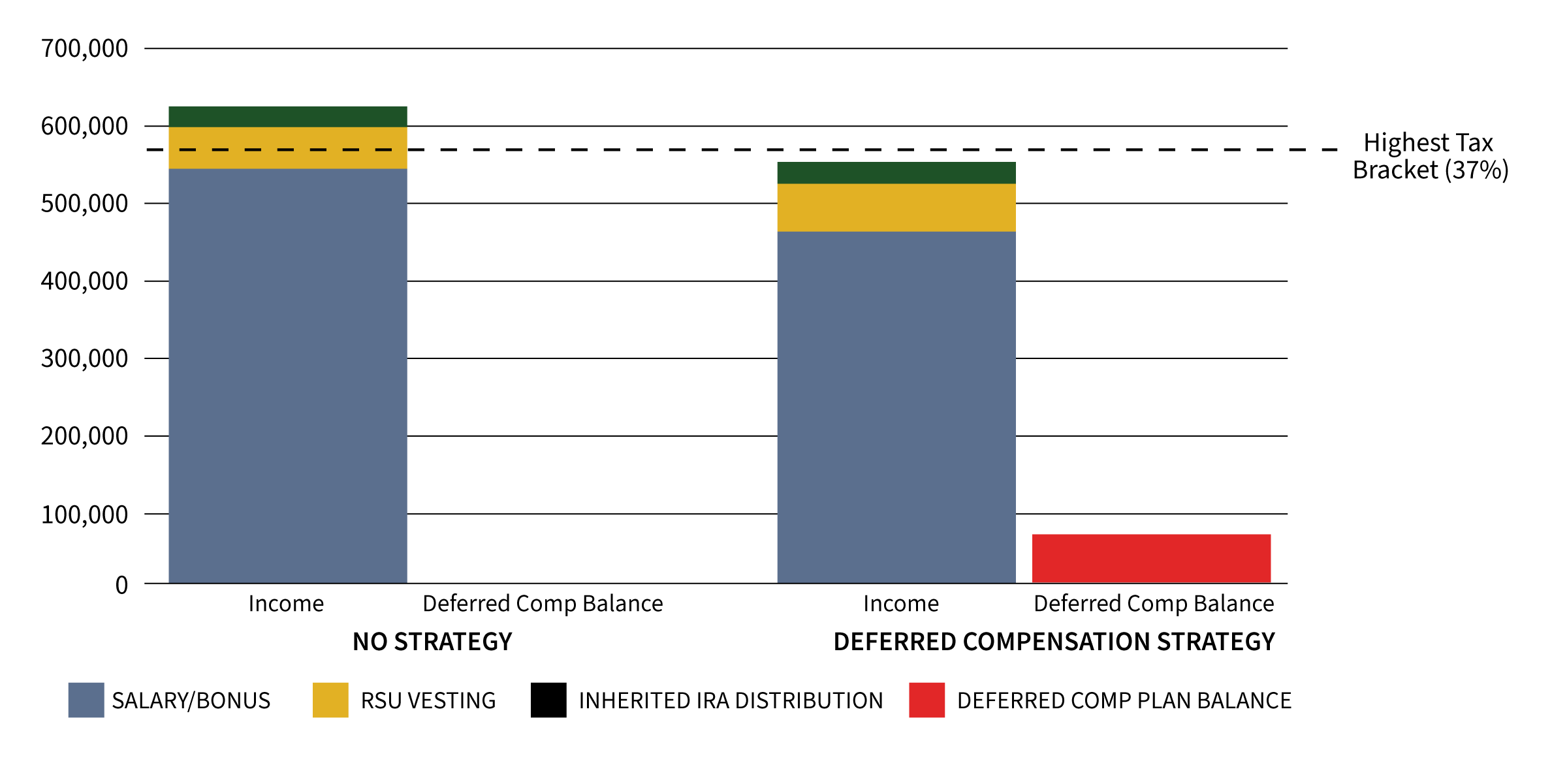

Gianna’s salary and bonus are $550,000 per year. She also receives stock compensation in the form of RSUs (restricted stock units), which, on average, is about $50,000 per year. RSUs are taxed as ordinary income when they vest, regardless of whether you sell the stock. She inherited an IRA from her father and is currently withdrawing $25,000 per year, which will continue for the next several years. This puts her total income at $625,000, placing her in the highest federal tax bracket. Keeping tax calculations simple for this example, Gianni would pay $187,636 in federal taxes. Making her effective tax rate 30.7%

Gianna does not need the additional $75,000 in income from the RSUs and IRA distribution, so she is losing a ton of money to taxes on income she will not be using right now. What can she do?

Because MetLife offers her a deferred compensation plan, she decides to defer $75,000 of her bonus each year. This will offset the amount she receives from the stock compensation and inherited IRA distributions.

Why would she do this? Look at the chart below.

As you can see, Gianna’s current plan puts her just over the threshold for the highest tax bracket. Deferring $75,000 of her compensation allows Gianna to reduce her taxable income to $550,000, keeping her just beneath the highest tax bracket. And her federal tax bill would be reduced to $160,690, saving her about $27,000 in federal taxes! This strategy allows her to maintain the same lifestyle spending, while the $75,000 she defers can be invested for retirement inside her NQDC plan.

If she continues this over the next ten years, that is an additional $750,000 in retirement savings, not including any investment growth. She can do this without spending any less or adjusting her lifestyle now. She’ll also realize the potential advantage of paying less in taxes because when she takes the distributions, she will be retired and in a lower tax bracket.

Strategy 2: Saving for Specific Goals

This strategy is simple and effective. All it takes is aligning your deferred compensation distributions with a specific goal in mind. This goal can be anything from your children’s education expenses to a down payment on a vacation home. Let’s look at how this concept works.

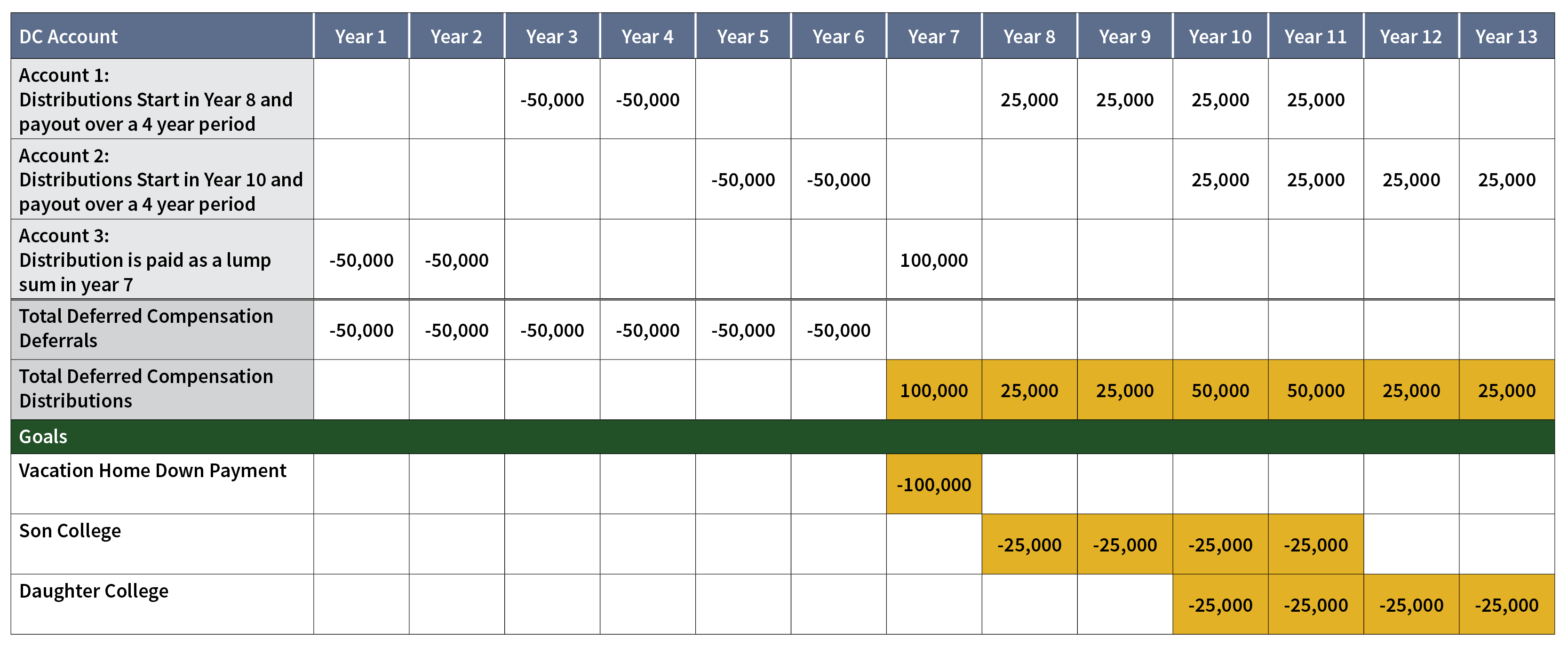

Bill and Laura have ambitious plans for their future. They want to make sure college expenses are covered for both children and purchase their dream vacation home. Their son will start college in eight years and their daughter in ten years, and they’d like to purchase their vacation home before the kids start college.

Cash flow is great for Bill and Laura right now. Bill has a deferred compensation plan through MetLife, and he developed a strategy to defer his salary over the next six years to fund the couple’s goals.

A common component of deferred compensation plans is the ability to have multiple accounts within the plan. Each account can have its own investment strategy and distribution schedule. When you make your elections, you decide which account you will be saving into. Bill’s plan at MetLife allows him to save into three different accounts inside his deferred comp plan.

As you can see from the chart, Bill created three accounts, each with a specific goal in mind. Account #1 will begin paying out in Year 8, over four years to pay for his son’s college. Account #2 will begin paying out in Year 10, over four years to pay for his daughter’s college. Account #3 will be paid out in a lump sum in Year 7 to cover the down payment on the vacation home.

Bill decides that deferring $50,000 per year into the accounts over the next six years will allow him to achieve his financial goals. Looking at the yellow boxes on the schedule, you can see that when distributions are made from the plan, they are each aligned with specific goals.

It’s important to note that we did not account for any investment growth in this example. This is something you should consider when determining if this strategy is right for you. Also, deferred compensation distributions are taxed as ordinary income, so being aware of what your total taxable income is likely to be at the time of distribution is also crucial.

Strategy 3: Filling the Income Gap until Social Security

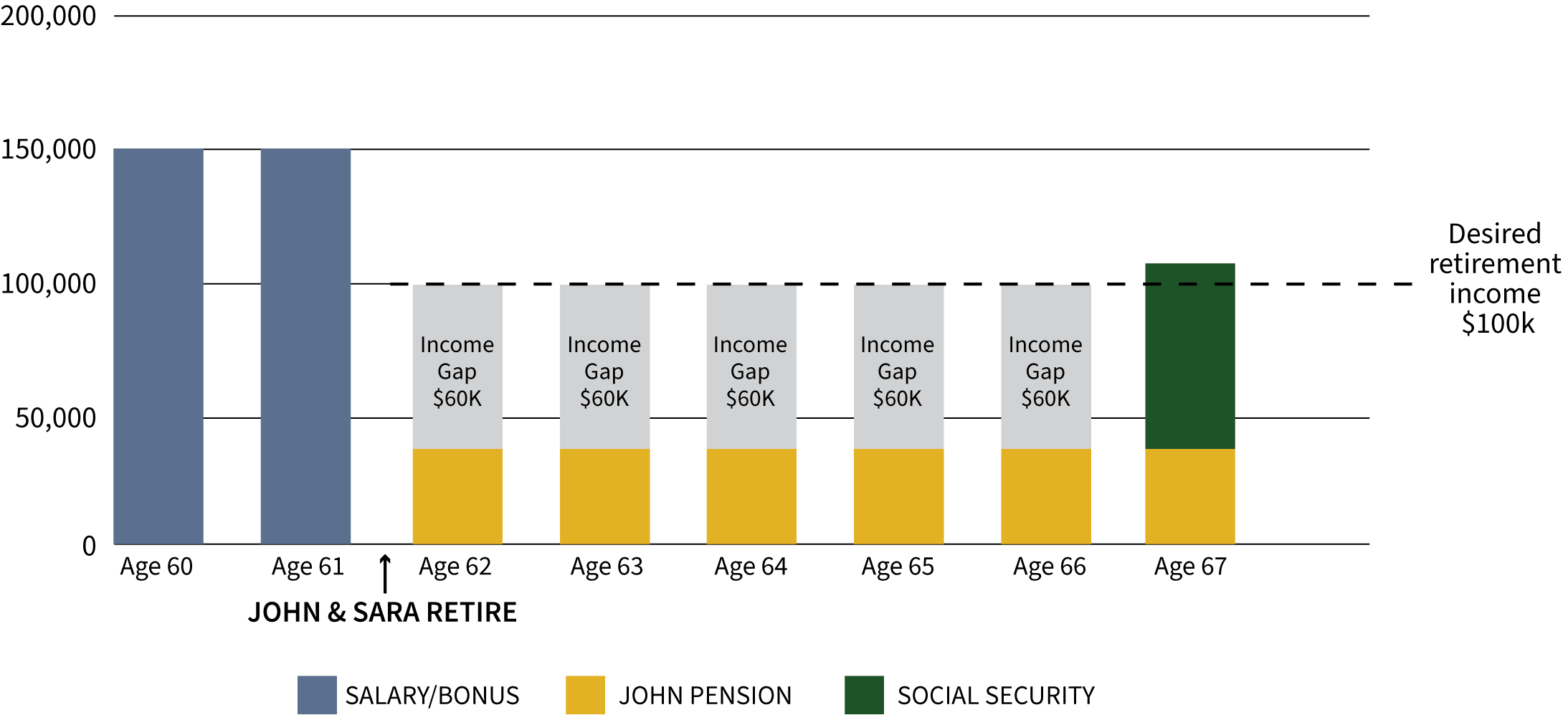

If you decide that you want to retire “early” or before age 65, the question you might be asking is, “Where will my income come from?” Most people rely on Social Security to supplement their income in retirement. But how does that work if you retire earlier than you would like to begin drawing SSI or before you become eligible?

John and Sara are a married couple who are both 60 years old. They plan to retire when they are 62 and would like to wait until 67 to take Social Security. John has a pension that will start when he retires at age 62.

This is what their projected income looks like right now:

You can see that John and Sara will have an income gap of $60,000 for the five years before Social Security kicks in. They will have to pull this from retirement accounts or other investments, which can lead to depleting assets sooner than anticipated.

You can see that John and Sara will have an income gap of $60,000 for the five years before Social Security kicks in. They will have to pull this from retirement accounts or other investments, which can lead to depleting assets sooner than anticipated.

Let’s examine an alternate scenario in which Sara utilizes her deferred compensation plan through MetLife. In this example, Sara defers 50% of her yearly bonus until retirement. The deferred compensation plan is to be distributed over five years, starting when Sara reaches age 62.

This is what their projected income looks like using Sara’s MetLife Leadership Deferred Compensation Plan:

The gap they previously had to make up is now filled by Sara’s distributions from her deferred comp plan. This has a significantly positive impact on their future because now the couple can let their retirement and investment assets continue to grow over the five-year period and use those gains later to supplement their income.

The gap they previously had to make up is now filled by Sara’s distributions from her deferred comp plan. This has a significantly positive impact on their future because now the couple can let their retirement and investment assets continue to grow over the five-year period and use those gains later to supplement their income.

It’s important to remember that a deferred compensation strategy like this needs to be reevaluated each year. There are a lot of moving parts to your plan; to stay on track, you need to adjust as needed constantly. For example, you may have some unexpected expenditures that affect your cash flow and may need more money in your paycheck instead of deferring that compensation later.

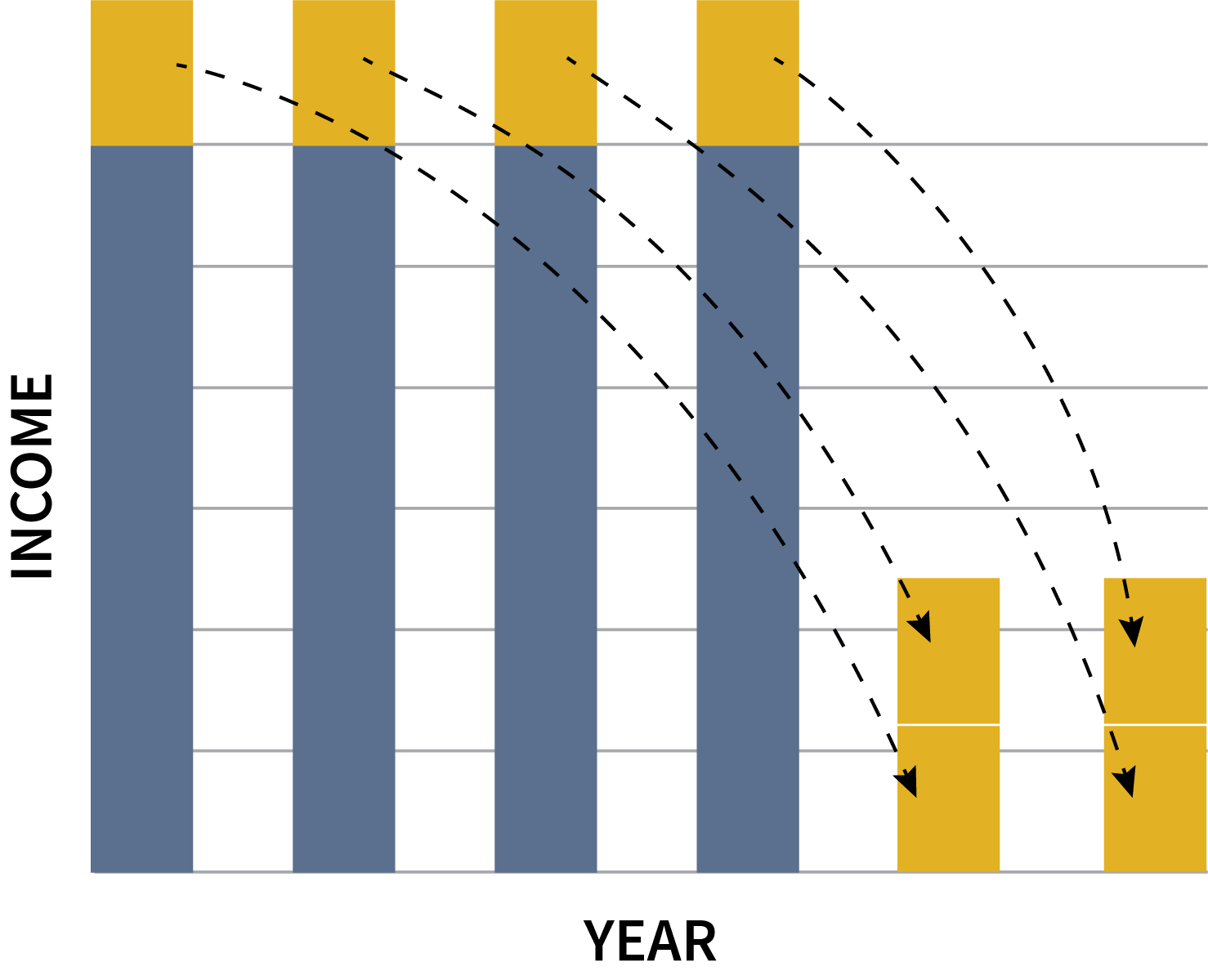

Strategy 4: Hedging for Getting Laid Off Early or Early Retirement

Let’s face it, companies go through layoffs and restructuring all the time. No employer, including MetLife, is immune to shifts in the economy, technological changes, or trends that lead to job losses. Unfortunately, the employees usually feel the most impact, especially the more highly compensated ones. Having a plan in place in the event you were to get laid off is essential to your financial well-being. The good news is if you have access to a deferred comp plan, it can be a great tool to hedge against uncertainty.

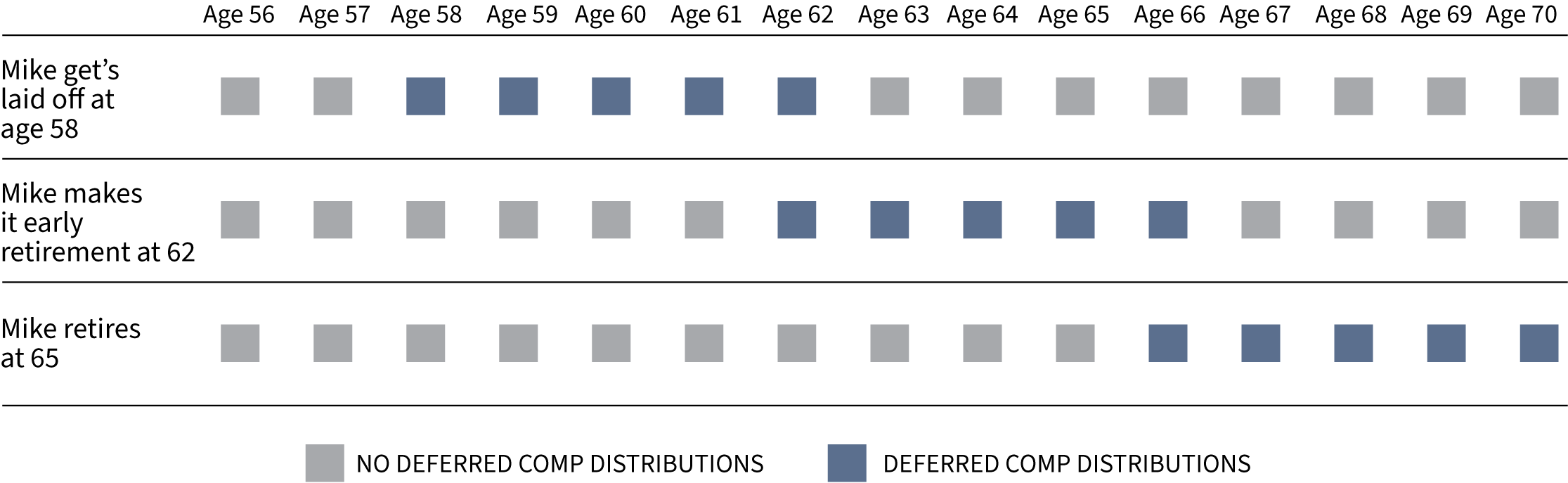

Let’s look at this in action. Mike has been a vice president at MetLife for the last ten years and is currently 55 years old. One of his major concerns is how an unexpected layoff would affect him and his family financially. To hedge against this possibility, he began deferring a portion of his bonus each year through his deferred comp plan. He set the distribution date as the day he separates or retires from the company, and the distributions will be paid out over five years. The current value of the plan is $350,000.

Looking at this chart, you can see that no matter when Mike leaves MetLife, he has a purpose for his deferred compensation. If he gets laid off at 58 (or any age, for that matter), the deferred comp will pay out over the next five years. Being that the current value is $350,000, that could be around $70,000 in income each year. This will allow him to buy some time while he looks for another job, or he could accept a job making less money since he has this income to supplement his pay.

Looking at this chart, you can see that no matter when Mike leaves MetLife, he has a purpose for his deferred compensation. If he gets laid off at 58 (or any age, for that matter), the deferred comp will pay out over the next five years. Being that the current value is $350,000, that could be around $70,000 in income each year. This will allow him to buy some time while he looks for another job, or he could accept a job making less money since he has this income to supplement his pay.

In the second scenario, Mike retires early at 62. He would receive his payout over the next five years until he is 66. The deferred compensation income would supplement his other retirement income until he takes Social Security. It could also pay for health insurance since he most likely would not be covered under his employer’s plan, and Medicare does not start until he is 65.

The last scenario has Mike retiring at the end of the year he turns 65, the longest he would continue working. If he’s able to stay that long, Mike could then use the deferred compensation to supplement his retirement income. This would enable him to withdraw less from his retirement and investment assets, allowing them to continue growing. He can also defer Social Security until 70 to max out his benefit since the MetLife Leadership Deferred Compensation Plan payout would supplement his income in the meantime. The point is that Mike would have a lot of options and flexibility.

Important Caveats

It’s important to remember that all the potential benefits of the MetLife Leadership Deferred Compensation Plan come with some risks. It’s essentially an I.O.U. from MetLife; if they go bankrupt, your deferred compensation contribution is considered unsecured debt and could be lost. If a significant portion of your wealth is also held in stock options and restricted stock units, relying heavily on deferred compensation could mean too much of your financial well-being depends on MetLife’s financial strength. Moreover, effectively leveraging deferred compensation plans requires careful thought and planning.

Keep in mind that NQDC plans have been dubbed “golden handcuffs” for a reason. As a highly compensated employee, your work is a valuable asset to MetLife as an employer, so the benefit is designed to incentivize retention. The more you make, the more you pay in taxes, and the more appealing the tax shelter is. If you intend to stay with MetLife, the financial advantages of using the plan strategically can be substantial and potentially well worth the carefully measured risk.

Defer, Don’t Delay

Deferred compensation is a potent tool that necessitates a thoughtful approach. Carefully weigh your options and proceed with cautious enthusiasm — sooner rather than later. Don’t delay putting the plan to work for your future; remember, time is valuable.

Decisions regarding the MetLife Leadership Deferred Compensation Plan should be intricately woven into the fabric of your comprehensive financial and retirement plans. Given the complexity and stakes involved, we recommend collaborating closely with a seasoned financial advisor familiar with the plan to help navigate the myriad possibilities and make informed choices aligned with your long-term goals.

As specialists in MetLife benefits and executive wealth planning, we offer a complimentary consultation to answer your deferred compensation questions. You can schedule a free session with our team here.

Strata Capital is a wealth management firm serving corporate executives, professionals, and entrepreneurs in the New York Tri-State Area, focusing on corporate benefits and executive compensation. Co-founded by David D’Albero and Carmine Coppola, the firm specializes in making the complex simple to ensure clients feel confident in their financial decisions. They can be reached by phone at (212) 367-2855, via email at carmine@stratacapital.co, or by visiting their website at stratacapital.co.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

This represents the views and opinions of Strata Capital and has not been reviewed or endorsed by MetLife or any of its employees. MetLife is not affiliated with Strata Capital and has not endorsed or approved their services.

This material was prepared by Crystal Marketing Solutions, LLC, and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate and is intended merely for educational purposes, not as advice.