By David C. D’Albero II

I often talk with people who believe they have a financial plan, but their “plan” is based more on assumptions and general ideas about their future than a structured strategy. Some people even use elaborate Excel spreadsheets to attempt to forecast what their assets will be worth and what their approximate expenses will be when they retire. These efforts, though commendable, do not equate to a comprehensive financial plan. While it’s true that most people have some form of planning in mind, a true financial plan that effectively prepares for the future involves a deeper, more structured approach.

What Is a Financial Plan?

A personal financial plan is a detailed guide that captures your financial goals, the strategies to pursue them, and the steps required along the way. This plan typically includes projections of your assets, liabilities, cash flow, and taxes to provide guidelines on how and where to save and invest.

In essence, a financial plan acts as a roadmap for managing your finances, helping you aim for stability and growth over the years. But to understand the true value of a professionally developed financial plan, it’s helpful to know exactly what it entails.

Key Components of a Personal Financial Plan

Financial Goals

- Short-term goals: Objectives achievable within a year, such as establishing an emergency fund or paying off credit card debt.

- Medium-term goals: Targets for the next 1-5 years, like saving for a house down payment or purchasing a car.

- Long-term goals: Plans extending beyond five years, including retirement savings and funding for children’s education

Overview of Your Current Financial Situation

- Income: A summary of all income streams, including salary, bonuses, and investment returns.

- Expenses: Itemized expenses categorized into fixed (such as rent or mortgage and utilities) and variable (like entertainment and dining out) using the needs, wants, and wishes classification system.

- Assets: An inventory of all assets, including cash, investments, and property.

- Liabilities: A comprehensive list of debts and financial obligations, such as loans, credit card balances, and mortgages.

Budgeting Strategies

- Budget Creation: Developing a detailed budget to monitor income versus expenses.

- Financial Optimization: Identify opportunities to cut costs and boost savings.

Managing Debt

- Debt Reduction: Implement strategies to accelerate the repayment of existing debts. This can include consolidating debt to a lower interest rate personal loan and paying the same amount to accelerate payoff or utilizing an introductory 0% card if you have the means to pay the debt off before the rate period expires.

- Debt Prevention: Establish practices to prevent or minimize new debt accumulation. Be careful with store credit cards, as they tend to have the highest interest rates. We generally recommend finding one credit card with the perks you like and using it for monthly expenses. This will make it much easier to track your monthly spending and avoid racking up debt.

Savings & Investment Strategies

- Emergency Fund: Establish a robust emergency fund to cover unforeseen expenses. The financial planning industry typically recommends saving around six months’ worth of expenses. However, there is no one-size-fits-all answer. Some people prefer to save a year’s worth of expenses, which is fine as long as it doesn’t compromise other financial goals.

- Goal-Specific Savings: Create dedicated savings accounts for specific objectives, such as retirement, children’s education, or purchasing a vacation home.

- Investment Planning: Develop investment strategies aligned with your timeline for utilizing the funds. For short-term goals, invest conservatively to avoid potential losses. Nothing would be more disheartening than finding the perfect home and then not being able to put in an offer because the stock market is down. For long-term goals, such as saving for your child’s college fund, take advantage of compounding interest and consider a more aggressive strategy initially, adjusting to conservative investments as you near your goal. This approach helps ensure your funds are available when needed while balancing the risk of short-term losses and the opportunity for long-term growth.

- Wealth Growth: To support wealth accumulation, construct a diverse investment portfolio that includes stocks, bonds, mutual funds, alternative investments like private equity and private credit, and rental real estate.

Maximizing Employee Benefits

- Retirement Plan Contributions: Maximize the company retirement plan match. Educate yourself on the matching program and understand how you can maximize what you receive. Some plans even match non-qualified savings plans.

- Deferred Compensation Usage: Leverage deferred compensation plans for tax efficiency and future savings.

- Stock Compensation Strategy: Develop strategies to optimize the benefits from stock compensation, aligning with overall financial goals. You can even utilize your deferred compensation to offset stock compensation if you have done good cashflow planning.

Insurance and Risk Management

- Risk Contingency Planning: Strategize for potential risks and uncertainties to safeguard financial stability. Examples of risks like this include premature death of yourself or your spouse, an illness or injury that prevents you from working, or even a layoff that results in an extended lapse in employment.

- Evaluation of Insurance Coverages: Evaluate the types of insurance your employer offers through the group benefits program and make sure to compare to options that can be purchased outside of your employer or accessed through your spouse’s benefits.

- Policy Acquisition: Obtain essential insurance coverage, including health, life, disability, property, and long-term care. You can use resources like lifehappens.org to help you figure the appropriate amount of coverage.

- Pro Tip – Keep Beneficiary Designations Up to Date: Beneficiary designations supersede a will in most cases, so make sure to review all of your beneficiaries to make sure they are still in line with your wishes.

Retirement Planning

- Goals: Define retirement objectives such as where will you live, what will you do, and what type of lifestyle you want, and determine how much it will cost on an annual basis.

- Accounts: Assess what types of accounts you have access to and whether they will be suitable for your savings plan. Some retirement accounts have limited access to investment choices. This can be especially dangerous for those nearing retirement who have accounts that have limited access to more conservative or income producing investment options. Make sure to evaluate accounts based on their contribution limits as well as their fees and investment choices.

- Contributions: Calculate necessary contributions to meet retirement objectives, then determine necessary savings amounts and locations.

Tax Optimization

- Tax Liability Assessment: Assess your current tax liabilities and identify which income sources generate the most taxes. Remember, not all income is taxed at the same rate.

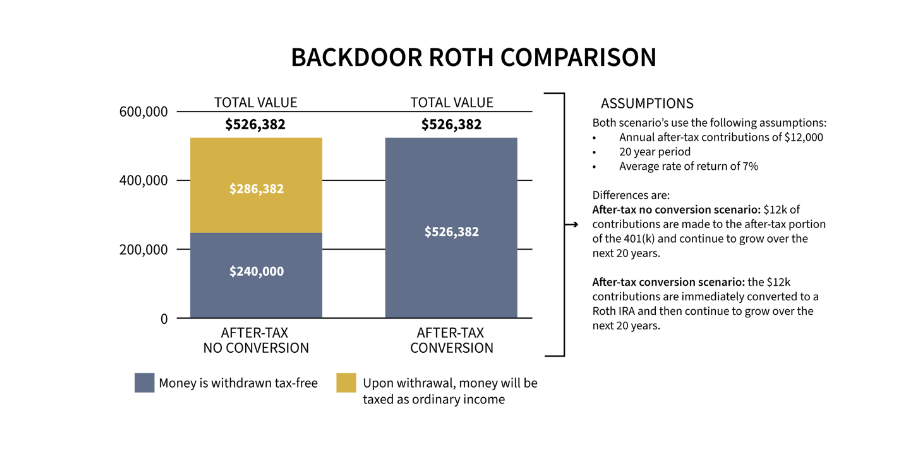

- Tax Reduction Strategies: Implement strategies to reduce taxes through deductions, credits, and tax-advantaged accounts. Evaluate the tools available to lower your tax liability, such as pre-tax 401(k) contributions, IRA savings (if you qualify), and deferred compensation. Also, review non-retirement investments to avoid unnecessary taxes. Properly managing funds can help minimize or even largely eliminate interest and capital gains taxes without sacrificing returns.

Estate Management

- Will and Trusts: Create or revise wills and establish trusts to manage and transfer assets effectively and efficiently,aiming to minimize complications for beneficiaries. Consult with an attorney who understands the rules in your state of residence.

- Tax and Legal Planning: Plan for potential estate taxes and understand legal considerations to ensure smooth asset transfer.

The Value of Professional Financial Planning

If it seems like a lot of plates to spin, it is. Attempting to DIY your financial plan with financial models in Excel is not only time-consuming but also risky. This is especially true when planning for retirement when there are no second chances.

Professional financial planners use sophisticated software to create projections and make recommendations, enhancing your chances of achieving your financial goals. They can also simulate various risks you could face down the line, providing a significant advantage by allowing you to prepare and adjust today, thus preventing potential financial crises in the future.

When it comes to DIY financial planning versus working with an experienced financial planner, I often put it this way, “I could represent myself in court, but I stand a better chance of winning if I bring an experienced attorney with me.”

Adapting and Refining Your Financial Plan

A mentor once told me, “Every financial plan ever written is wrong.” This wasn’t a critique of financial planning but a recognition that life is dynamic—goals shift, incomes fluctuate, liabilities change, and financial regulations like contribution limits and tax brackets are updated. This makes financial planning a continual process, not a one-time event.

The initial financial plan is crucial for setting your trajectory, but true financial optimization requires regular adjustments. If you’re working with a financial planner, it’s advisable to meet at least twice a year to review and refine your strategy.

When choosing a financial planner, selecting someone whose expertise aligns with your specific needs and specializes in working with people of similar background and net worth is important. Just as you wouldn’t hire a traffic court attorney to handle a real estate closing or consult a foot surgeon about heart issues, choosing a financial planner experienced in managing scenarios similar to yours can make a significant difference in effectively managing your wealth.

Are You Ready to Work with a Financial Advisor?

If you’re just starting out, you might be able to handle your own financial planning for now. There are plenty of great resources online if you know where to look (hint: check out www.stratacapital.co).

If you’re managing your own financial planning, here are two key pieces of advice:

- Don’t blindly follow what your friends are doing just because you don’t know what to do. It’s common to see young professionals investing in the same funds as their older coworkers without fully understanding the implications.

- Don’t hesitate to admit when you don’t understand something, and seek professional advice. There are many trustworthy and knowledgeable financial planners who can guide you in the right direction.

If you think it might be time to work with a professional financial advisor to begin your comprehensive financial planning process, contact us for a consultation.

Strata Capital is a wealth management firm serving corporate executives, professionals, and entrepreneurs in the New York Tri-State Area, focusing on corporate benefits and executive compensation. Co-founded by David D’Albero and Carmine Coppola, the firm specializes in making the complex simple to ensure clients feel confident in their financial decisions. They can be reached by phone at (212) 367-2855, via email at carmine@stratacapital.co, or by visiting their website at stratacapital.co.

Cornerstone Planning Group, Inc., (“CSPG”) is an SEC registered investment advisory firm. The information contained herein should not be construed as personalized investment advice and should not be considered as a solicitation for investment advisory service. The information (e.g., tax ) provided is believed to be accurate however CSPG does not guarantee or otherwise warrant such information. For more information regarding CSPG you can refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov) and review our Form ADV Brochure and other disclosures.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

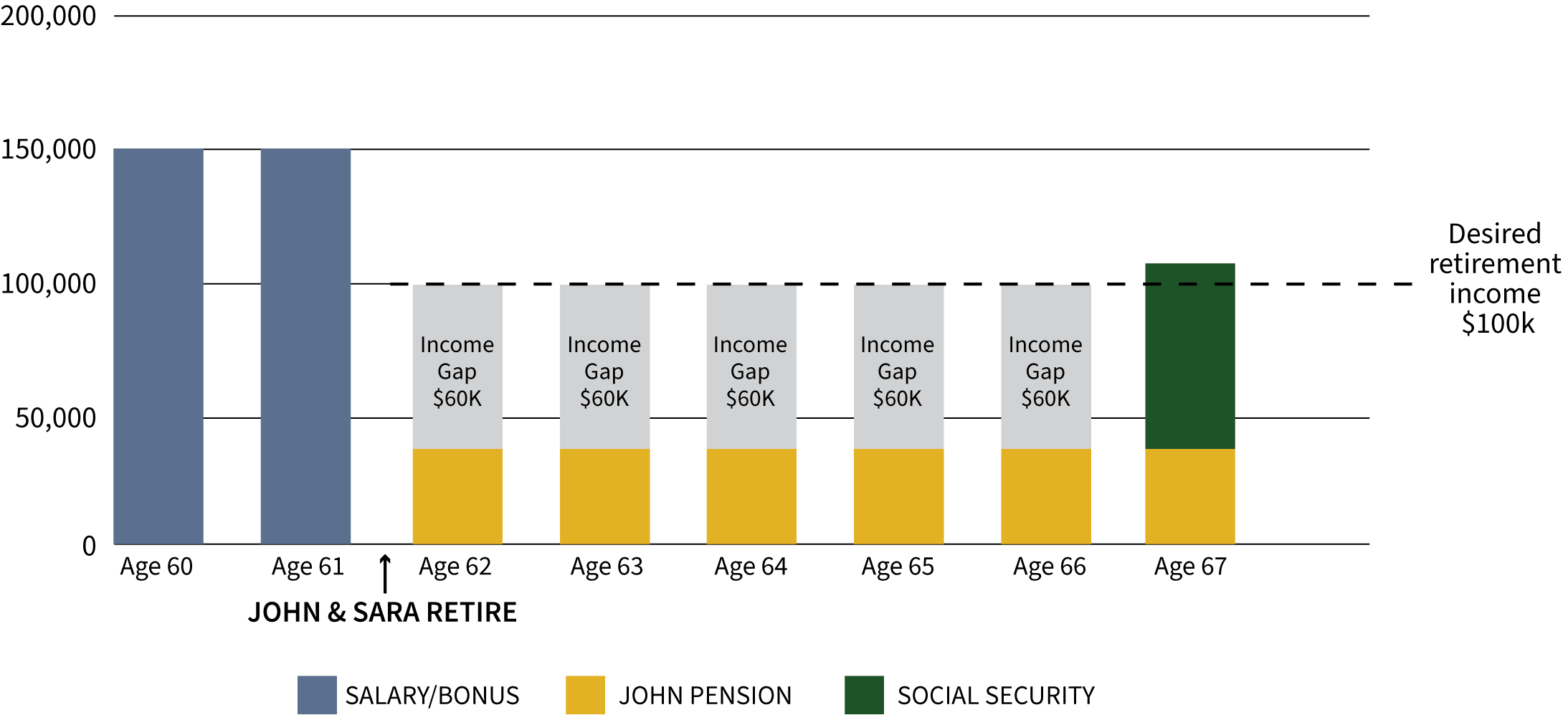

You can see that John and Sara will have an income gap of $60,000 for the five years before Social Security kicks in. They will have to pull this from retirement accounts or other investments, which can lead to depleting assets sooner than anticipated.

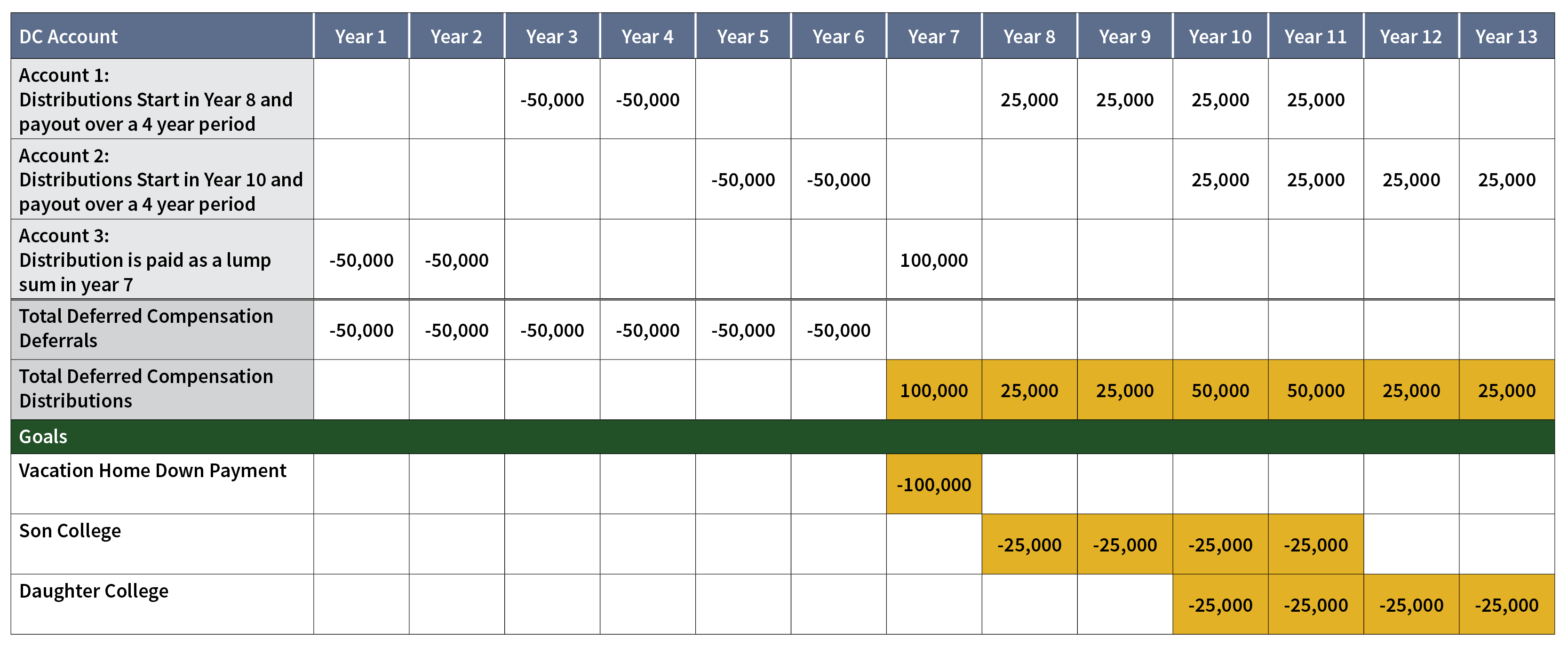

You can see that John and Sara will have an income gap of $60,000 for the five years before Social Security kicks in. They will have to pull this from retirement accounts or other investments, which can lead to depleting assets sooner than anticipated. The gap they previously had to make up is now filled by Sara’s distributions from her deferred comp plan. This has a significantly positive impact on their future because now the couple can let their retirement and investment assets continue to grow over the five-year period and use those gains later to supplement their income.

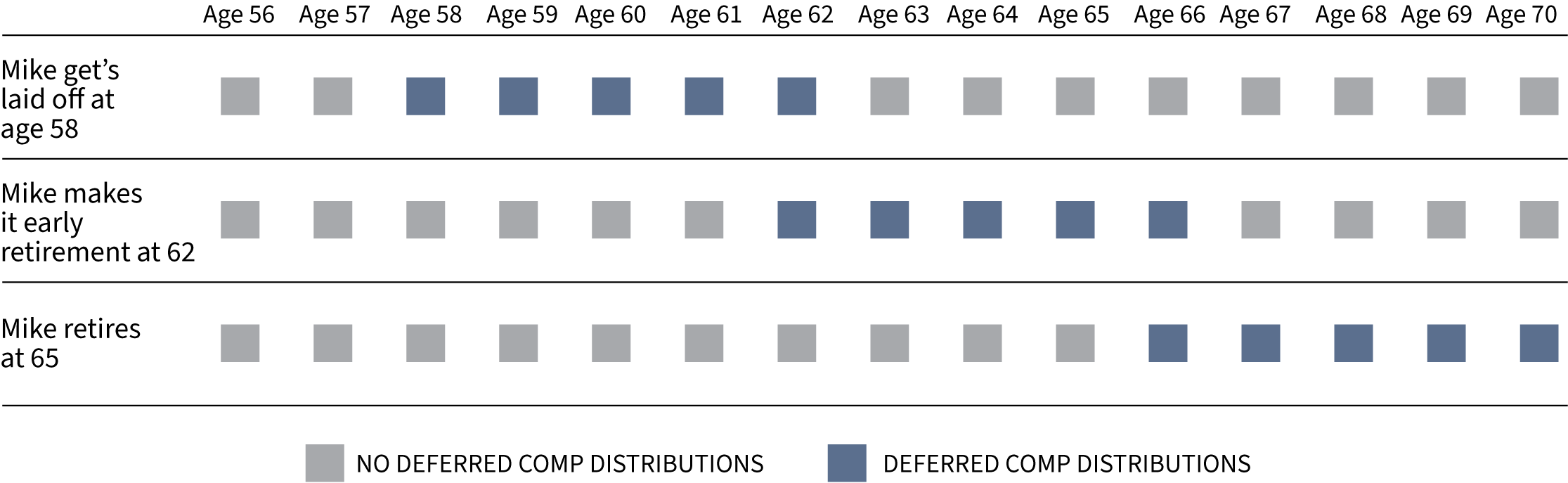

The gap they previously had to make up is now filled by Sara’s distributions from her deferred comp plan. This has a significantly positive impact on their future because now the couple can let their retirement and investment assets continue to grow over the five-year period and use those gains later to supplement their income.  Looking at this chart, you can see that no matter when Mike leaves MetLife, he has a purpose for his deferred compensation. If he gets laid off at 58 (or any age, for that matter), the deferred comp will pay out over the next five years. Being that the current value is $350,000, that could be around $70,000 in income each year. This will allow him to buy some time while he looks for another job, or he could accept a job making less money since he has this income to supplement his pay.

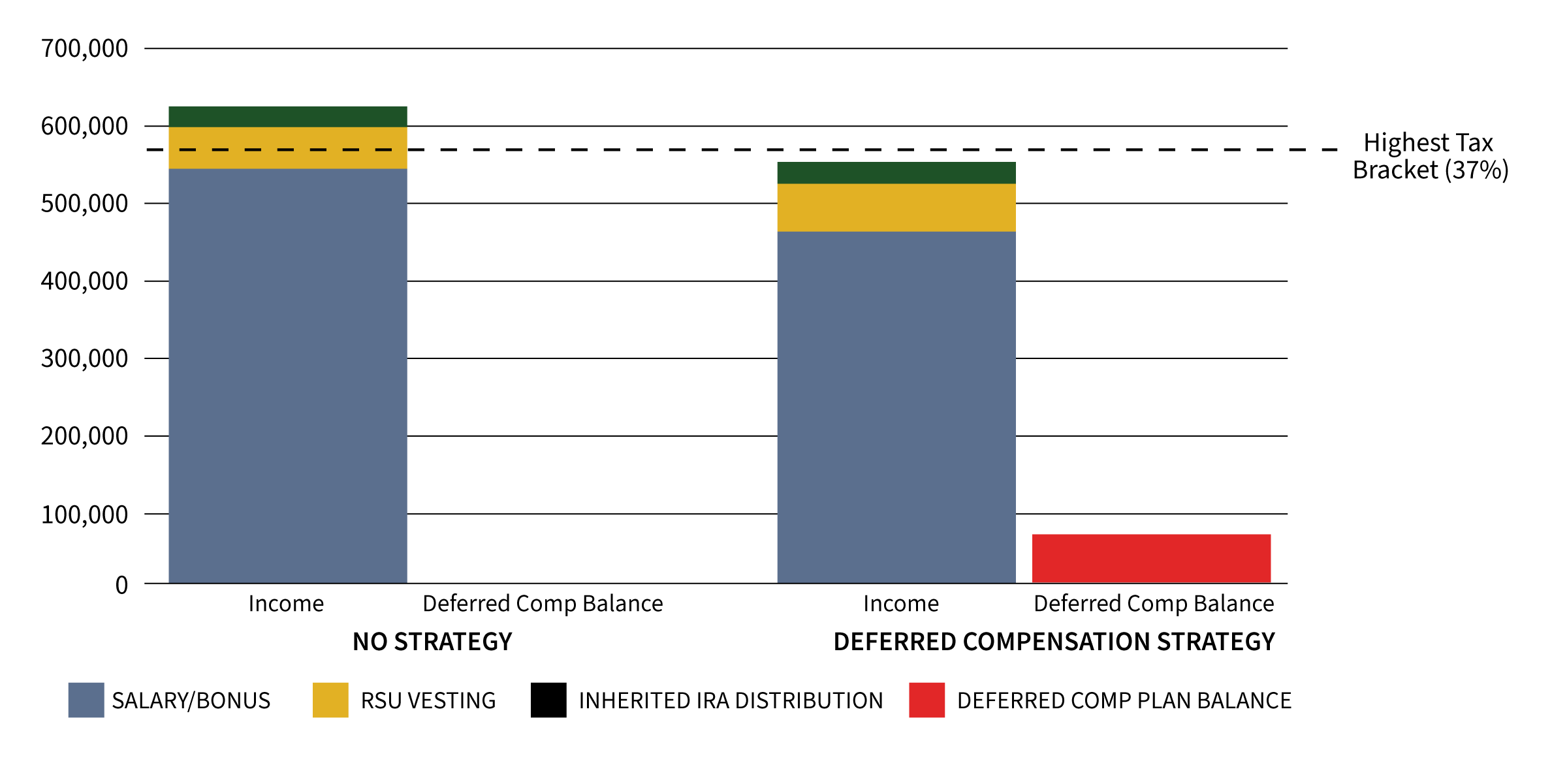

Looking at this chart, you can see that no matter when Mike leaves MetLife, he has a purpose for his deferred compensation. If he gets laid off at 58 (or any age, for that matter), the deferred comp will pay out over the next five years. Being that the current value is $350,000, that could be around $70,000 in income each year. This will allow him to buy some time while he looks for another job, or he could accept a job making less money since he has this income to supplement his pay.