By David C. D’Albero, Co-Founder, Strata Capital

There’s a growing tension that many successful executives feel today. You want to maximize Roth contributions for long-term tax-free growth, but you’re also aware of the tax benefits that come from traditional pre-tax savings. It often feels like you have to choose between future benefit and present-day tax relief.

That tradeoff might not be necessary.

For high-income professionals with access to a nonqualified deferred compensation plan, there is a little-known strategy that can unlock the best of both worlds. It is what we call at Strata, the Double Roth Max. This approach lets you maximize your Roth contributions while still reducing your current taxable income, using the tax shelter of your deferred compensation plan.

This is not a beginner tactic. It requires the right plan design and strong cash flow. For executives with complex compensation packages, it can be one of the most powerful retirement strategies available.

Let’s break down how it works.

Step 1: Max Out Your Roth 401(k) Contributions

Start by contributing the full annual limit to your Roth 401(k). In 2025, that was $23,500. If you’re 50 or older, you qualify for an additional $7,500 catch-up contribution, bringing your total to $31,000.

For those between ages 60 and 63, the numbers get even better. Under the Secure Act 2.0 rules, you are eligible for a special catch-up of $11,250. This allows you to contribute up to $34,750 to your Roth 401(k) in 2025.

That is the first layer of the strategy, and it is already powerful on its own.

Step 2: Add After-Tax Contributions to Hit the 401(k) Limit

Next, take advantage of your plan’s after-tax contribution feature. The total 401(k) contribution limit for 2025 was $70,000. This includes both employee and employer contributions.

Once you have hit the Roth 401(k) limit and factored in any employer match, you can fill the remaining gap with after-tax dollars.

Let’s say your employer match is $10,000 and you have already contributed $23,500. That gives you room to contribute another $36,500 in after-tax dollars to reach the $70,000 limit.

Not every plan allows this, so review your plan documents carefully or consult your benefits team.

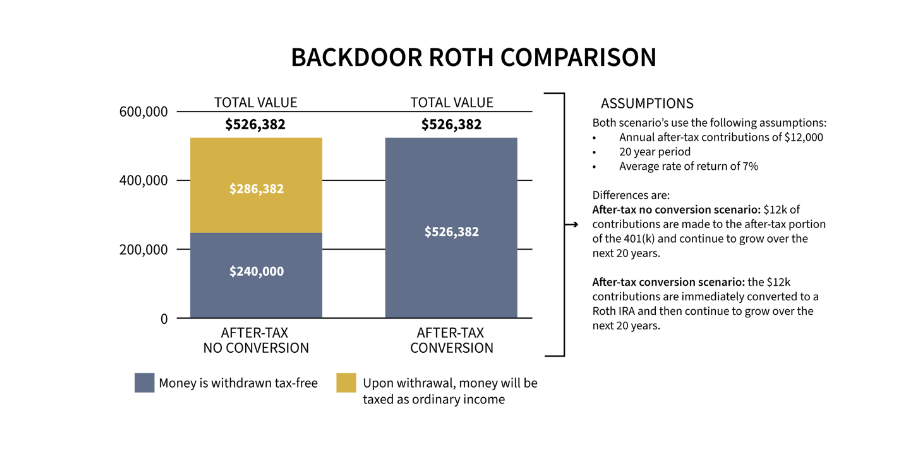

Step 3: Execute a Mega Backdoor Roth Conversion

Once you make those after-tax contributions, convert them to a Roth account. This can be done either within the plan or by rolling them into a Roth IRA. This converts your after-tax contributions into Roth dollars that can grow and be withdrawn tax free in retirement.

Ideally, this conversion happens quickly to limit any taxable growth.

Used correctly, this step can add another $30,000 to $46,500 to your Roth portfolio, depending on your age and employer match.

Step 4: Shift Your Tax Deduction to Deferred Compensation

Here is the part that sets the Double Roth Max apart.

By focusing on Roth and after-tax contributions, you are giving up the current-year tax deduction that comes with traditional pre-tax 401(k) contributions. That would be a dealbreaker for many.

Instead, shift that tax deduction into your company’s deferred compensation plan. By deferring a portion of your salary into an NQDC plan, you reduce your taxable income in the current year, similar to how a traditional 401(k) works.

In other words:

- You are building tax-free Roth income for the future.

- You are still getting a tax deduction today.

- You maintain control over how and when that deferred income is paid.

This structure supports both short-term efficiency and long-term growth.

What the Numbers Could Look Like

Here’s a hypothetical example for a 61-year-old executive:

- $34,750 contributed to the Roth 401(k)

- $35,250 contributed after tax and converted via mega backdoor Roth

- Total Roth contributions: $70,000

- $50,000 deferred into the company’s NQDC plan for a current tax deduction

This structure helps reduce this year’s tax liability while aggressively building tax-free income for retirement.

Who This Strategy Works For

The Double Roth Max works best for professionals who:

- Earn well above the IRS income limits for Roth IRA eligibility

- Have access to a strong nonqualified deferred compensation plan

- Are already maxing out their standard 401(k) contributions

- Want more of their wealth in tax-free vehicles

- Can manage short-term cash flow while pursuing long-term growth

If you check these boxes, this strategy could dramatically improve your retirement plan.

What to Watch Out For

There are several technical elements that must be coordinated:

- Not all plans allow after-tax contributions or in-plan Roth conversions

- Timing is important to avoid tax consequences on after-tax growth

- NQDC plans vary widely, and each one has its own rules and limitations

- Strong cash flow is required to support simultaneous contributions and deferrals

As always, work with a knowledgeable advisor, CPA, and benefits administrator to ensure you are executing this strategy correctly.

The Strategy Behind the Numbers

At this level, retirement planning is not just about maxing out contributions. It is about aligning your compensation structure, tax profile, and investment goals into a coordinated plan.

The Double Roth Max gives high earners a rare opportunity to contribute significantly more into Roth accounts without sacrificing near-term tax efficiency.

That combination is hard to find. When implemented correctly, it can result in a more balanced portfolio, reduced tax drag, and greater control over your future income.

Want the Full Walkthrough?

In my latest video, I break down the full Double Roth Max strategy using real-world numbers and practical guidance.

Watch it here: Give me 2 minutes… I’ll add $100k/yr to your investments

You will learn:

- How to structure your contributions

- What plan features are required

- Where high-income earners can find the most leverage

If you are looking to take your planning to the next level, this is a strategy worth exploring.

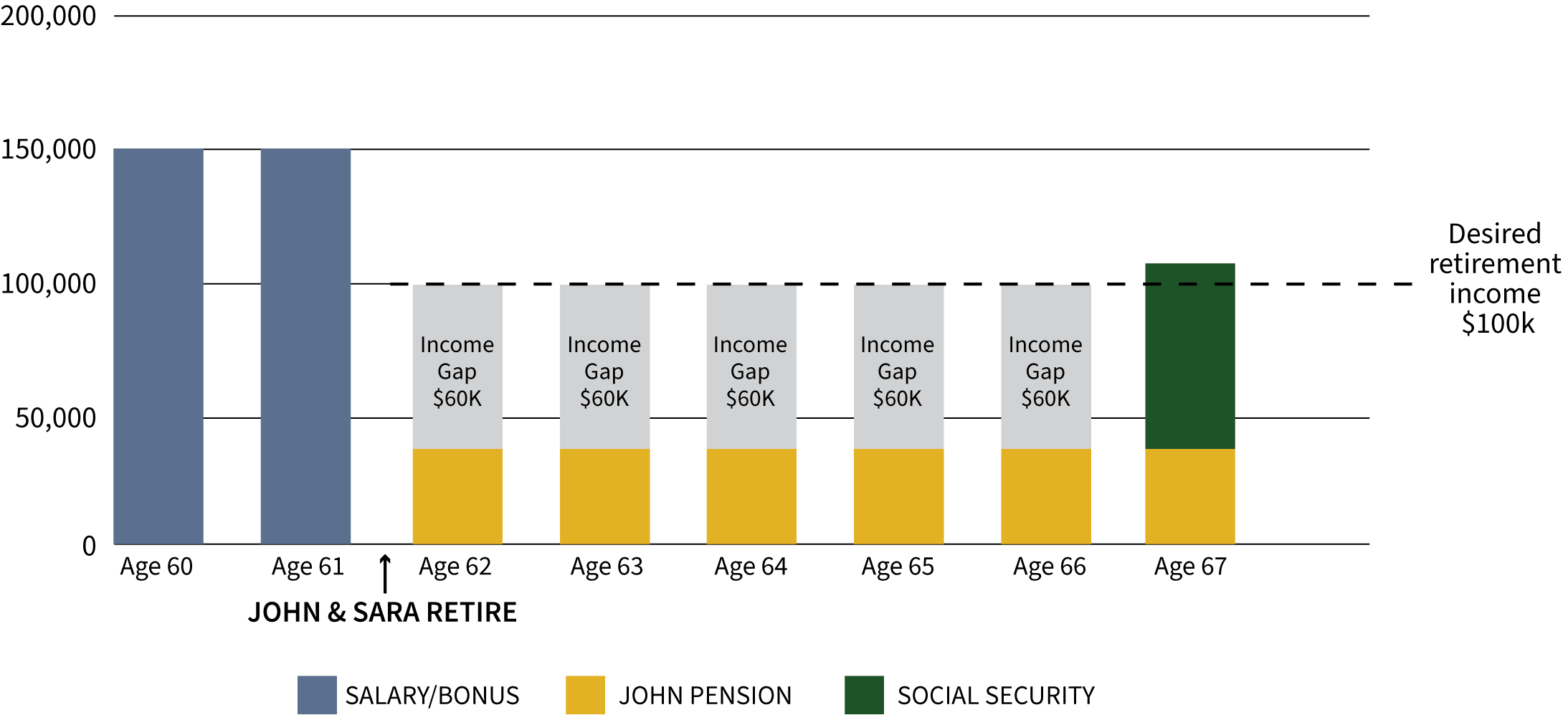

You can see that John and Sara will have an income gap of $60,000 for the five years before Social Security kicks in. They will have to pull this from retirement accounts or other investments, which can lead to depleting assets sooner than anticipated.

You can see that John and Sara will have an income gap of $60,000 for the five years before Social Security kicks in. They will have to pull this from retirement accounts or other investments, which can lead to depleting assets sooner than anticipated. The gap they previously had to make up is now filled by Sara’s distributions from her deferred comp plan. This has a significantly positive impact on their future because now the couple can let their retirement and investment assets continue to grow over the five-year period and use those gains later to supplement their income.

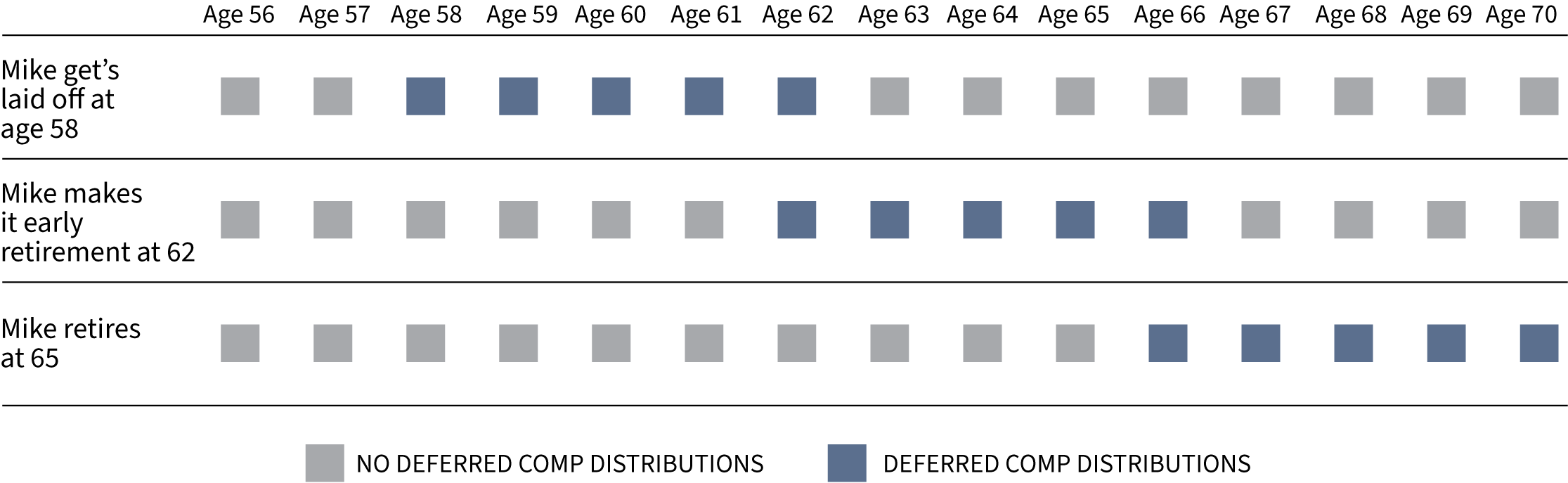

The gap they previously had to make up is now filled by Sara’s distributions from her deferred comp plan. This has a significantly positive impact on their future because now the couple can let their retirement and investment assets continue to grow over the five-year period and use those gains later to supplement their income.  Looking at this chart, you can see that no matter when Mike leaves MetLife, he has a purpose for his deferred compensation. If he gets laid off at 58 (or any age, for that matter), the deferred comp will pay out over the next five years. Being that the current value is $350,000, that could be around $70,000 in income each year. This will allow him to buy some time while he looks for another job, or he could accept a job making less money since he has this income to supplement his pay.

Looking at this chart, you can see that no matter when Mike leaves MetLife, he has a purpose for his deferred compensation. If he gets laid off at 58 (or any age, for that matter), the deferred comp will pay out over the next five years. Being that the current value is $350,000, that could be around $70,000 in income each year. This will allow him to buy some time while he looks for another job, or he could accept a job making less money since he has this income to supplement his pay.